I was at Tinubu Square, a popular place in Lagos Island, Nigeria, to do some business, and somehow, I decided to have a haircut while waiting.

While sitting in the chair, a group of guys walked in. I paid no attention to them until I heard a loud voice behind me in typical Nigerian Pidgin:

“Omo, the stock wey I buy don go up 60%.”

(Wow. The stock I bought has gone up 60%.)

I looked in the mirror in front of me to catch a glimpse of the guy who said it, and just then, another of them said:

“My own never too go up. Na just 13%.”

(My own is not up by much. Only 13%.)

I told my barber to wait, turned the swinging chair and asked them, like a student who has seen his Sensei: “Please, which stocks? When did you buy? How do I get in?”

For the first time in over four years, I got to know that my trusted barber didn’t really like cutting hair. He was just in it for the money. We left my hair and sat together as we got schooled on how to join communities that share weekly stock picks, how to buy stocks whose prices have not gone above 1 naira in ages, and a lot more ‘expert tips’ on becoming ‘successful investors’.

No one in the circle knew I had a bit of exposure to the financial market, but after the conversation, I knew deep within that the NGX article needed to take priority over my upcoming IPO masterpiece.

Truth is, I don’t fear when a few people are making money. I fear when everyone is making money. That little conversation left me thinking of the NGX beyond the financial models and calculations.

Why I Wrote This. TL;DR

History does not repeat itself, but it often rhymes. I see a lot of striking parallels between the NGX now and in 2007. Back then, economic reforms helped Nigeria earn a BB-rating, which led to US$18bn debt write-off and created pension funds that have several billions of Naira to be invested in Nigerian securities. Banks were also at the heart of the rally, and stocks were being hawked in every nook and cranny of the country.

It’s not like-for-like (no margin lending), but the case is not really different now. Economic re-rating, pension funds, banking consolidation, and an insatiable hunger for stocks from retail investors. Plus, we now have a massive IPO on the way. We might not see a full-blown crash like 2007-08, but ignoring a correction is not the smartest move.

If you close the article now, you’ve gotten the full picture already. You might just need to know the fine details below.

How Large-Scale Players Defined the Current Bull Run

The best way to gauge the performance of the Nigerian stock market is the All-Share Index (ASI). Over the first four months of 2026, the ASI rocketed over 55%, as the NGX added an astonishing ₦56.6 trillion in market capitalization.

However, my barber’s friends and the retail crowd just arriving at the party didn’t build this foundation. Institutions did.

A short trip to 2023 shows the start of a very interesting story. Nigeria was added to the FATF Grey List in February, and by September, FTSE Russell downgraded the NGX to “Unclassified” – effectively deleting it from global indices at zero value due to foreign exchange repatriation blockages. The Nigerian stock market was literally dead money.

Then, a perfectly sequenced line-up of structural catalysts cleared the wreckage.

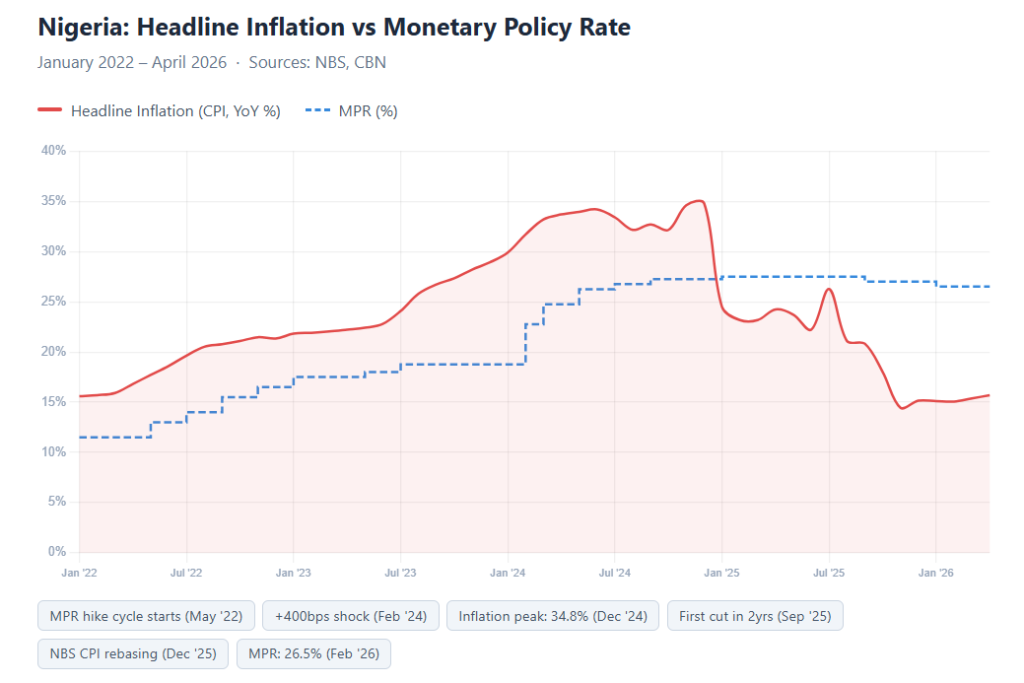

First, Inflation peaked at 34.8% in December 2024 and began falling hard. Next, Nigeria completed its 19 FATF action plans in May 2025, culminating in its official removal from the Grey List in late October 2025.

This, with the CBN clearing the FX backlog, paved the way for the FTSE Russell to officially announce Nigeria’s upgrade back to Frontier Market status.

Nigeria Capital Markets · Structural Recovery

From Grey List to Re-Rating:

The 2023–2026 StoryNGX All-Share Index — actual points (selected dates)

Key events — chronological

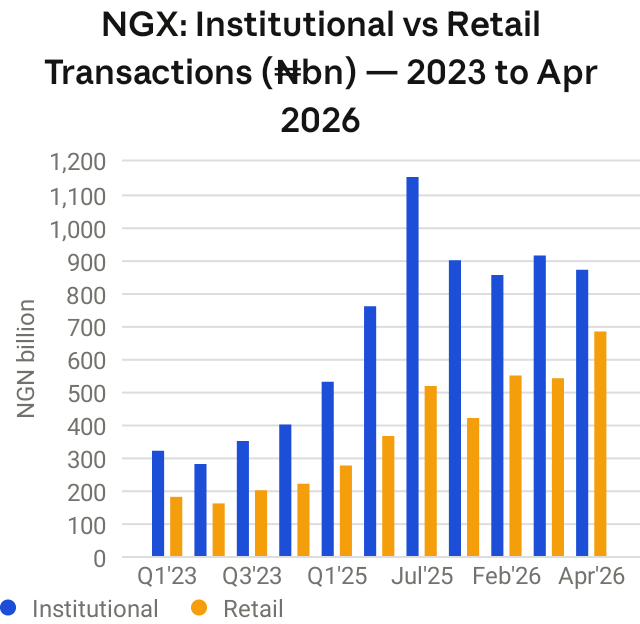

Institutions noticed first. While retail transactions barely flinched mid 2025, institutional trading volume surged by nearly 50%.

Someone might ask: but these are institutional transactions, not institutional buys. How sure are we that these were not Institutions selling? Well, there’s a very solid point there, and further supporting the fact that we don’t have a public ticker tracking net institutional buys. However, the National Pension Commission (PenCom) report gave away the game: Pension Fund Administrators (PFAs) were aggressively expanding their domestic equity allocations to outpace inflation.

The Divergence: Retail FOMO Meets Institutional Caution

The retail crowd didn’t catch on until early 2026. (June 2025 was an anomaly for both retail and institutions). In February, retail transaction volume exploded past ₦548 billion as everyday investors finally noticed the historic index highs.

Fastforward to April, retail transactions hit ₦683 billion, a 26% increase MoM, but the major point was what institutions were doing. Over the same time frame, institutional investors’ transactions reduced by 4.69%.

Even if they’re net buys, a zoom out to the start of the year shows Institutional transaction values have trended flat-to-declining, even as retail volumes hit successive record highs.

Institutional Exit: Passing the Bag to Retail

The tables aren’t turning because institutions are going to dump their heavy large-cap holdings like Dangote Cement or BUA onto retail liquidity. Rather, it’s more about the mechanics that ‘forced’ institutions to buy equities naturally expiring. The unwinding is fuelled by three main triggers

1. The Rebirth of the Fixed-Income Alternative

With headline inflation aggressively cooling toward 15% and the Monetary Policy Rate (MPR) sitting highly restrictive at 26.5%, the Nigerian financial ecosystem has crossed into a strong positive real yield environment. In 2024 and 2025, PFAs were forced into equities because holding cash meant watching assets burn under 34% inflation.

Today, a risk-free FGN bond or Treasury Bill yields a guaranteed real profit. The move away from equities will be fueled by rising real yields on FGN bonds, and T-bills are making the fixed-income sleeve of PFA portfolios genuinely competitive again for the first time in two years.

2. The Exhaustion of the FTSE Inflow Pipeline

The global frontier market funds that mechanically re-weighted Nigerian large-caps into their portfolios operate on strict quarterly tranches. That buying is finite. Once international asset managers hit their regulatory target weights, that aggressive, non-price-sensitive buying ends. BlackRock and Vanguard are not buying because they love the country. They buy in tranches because they are mandated to. Plus the fact that their purchases are aggressive and not price sensitive could trick retail into thinking this is an insatiable, endless bull run.

3. The Normalization of Corporate Earnings

The explosive banking sector earnings that justified early multiple expansions were heavily padded by high emergency interest margins and one-time foreign exchange revaluation gains. As the Naira stabilizes and the central bank prepares to eventually ease rates, these cyclical windfalls will naturally flatten out.

Impact of Dangote Refinery IPO on the NGX

All eyes are on the Dangote Refinery IPO. It is undoubtedly grand, with a 10% float at about a $50 billion valuation. This not only put it as the biggest IPO in African history, but the resulting $5 billion capital call is structurally larger than the five biggest African IPOs in history put together.

Largest Traditional IPOs on African Exchanges — vs Dangote Refinery

Primary share sales on African stock exchanges · USD millions · New shares issued to public investors

To the untrained eye, this is a perfect setup for a bullish run continuation.

While analysing the IPO, I asked myself one question. Has Nigeria, or even Africa, had any high-stakes IPO to measure the Dangote refinery IPO with? Not really.

You could say MTN Nigeria… But it was a listing by introduction, not an IPO. Someone else comes and says Vodacom, but it arrived by a Pre-Listing Statement and unbundling from Telkom.

The sheer magnitude of what Aliko Dangote is bringing on board is truly a one-of-one. So, how are most online analysts so sure it will be a catalyst for the next leg of the bullish run?

I looked beyond Africa to find a global benchmark. Even on Wall Street, there wasn’t a template that truly matched this specific dynamic.

After many days, I found it – The only company globally that mirrors the exact structural gravity of the Dangote Refinery IPO is a trillion-dollar behemoth: Saudi Aramco.

The similarities between the two are glaring. Both hold a monumental scale relative to their local domestic exchanges; both represent the privatization or public transition of critical national energy infrastructure; and both were designed as crown-jewel catalysts for their local capital markets.

Saudi Aramco IPO vs Dangote Refinery IPO

| Theme | Saudi Aramco · 2019 | Dangote Refinery · 2026 | |

|---|---|---|---|

| 01 | First-ever public listing of a national energy giant | Aramco 80+ years of state ownership. Listed once, in 2019. |

Dangote Decade-long private build. No prior public ownership. |

| 02 | Controlling party retains near-total ownership post-IPO | Aramco Saudi government kept 98.5%. Tiny public float. |

Dangote At most 10% sold. Aliko Dangote retains full strategic control. |

| 03 | Founder valuation exceeds independent analyst estimates | Aramco MBS sought $2trn. Banks said $1.2trn. It priced near the low end. |

Dangote Cited at $40–50bn now. Was $20–25bn a year ago. |

| 04 | Domestic retail investors targeted as primary demand base | Aramco Saudi retail and government funds anchored the offer. |

Dangote NGX listing built for Nigerian retail investors and pension funds. |

| 05 | All operational risk concentrated in a single location | Aramco Value tied to a small number of super-giant fields in the Kingdom. |

Dangote 650,000 bpd, all revenue, all risk. One site in Lekki. |

| 06 | IPO framed as proof of national economic transformation | Aramco Inseparable from Vision 2030. Sovereign credibility on the line. |

Dangote Positioned as Nigeria’s industrial coming-of-age. “The golden stock.” |

| 07 | Returns structurally tied to one commodity cycle | Aramco Share price tracks Brent crude. Operational strength is secondary. |

Dangote Margins, dividends, and exports all move with the crude-to-product spread. |

The question I then asked myself was: Did the Saudi Aramco IPO crash the Tadawul (Saudi Arabia’s Stock Exchange)?

The answer was as clear as day. In the months leading up to the IPO, the Tadawul All Share Index actually fell, wiping out most of its yearly gains. Domestic retail investors and institutional fund managers began aggressively dumping their shares in other blue-chip companies (like Al Rajhi Bank and SABIC) to hoard cash so they could subscribe to the Aramco IPO.

The Saudi government realized the risk of such a massive IPO and deployed unprecedented, aggressive interventions to protect the local exchange from a massive liquidity drain.

1. Scaling Down the Float

The original plan was to float 5% of the company globally to raise $100 billion. Realizing the local market could never absorb that without a catastrophe, they scaled the local listing down to just 1.5% of the company, bringing the local capital call down to about $25.6 billion.

2. Engineering Domestic Demand via Credit

To ensure local investors didn’t have to completely liquidate the rest of their stock portfolios to participate, Saudi banks were instructed to offer unprecedented, cheap leverage. Retail investors were given leverage ratios of up to 2-to-1 (borrowing exactly what they put down) to buy Aramco shares.

3. The “Patriotic Duty” Capital Call

The government heavily leaned on wealthy Saudi merchant families and regional sovereign funds to buy and hold the stock, keeping international short-sellers out of the initial equation.

4. Capping Index Weight

To prevent Aramco from completely dictating the direction of the entire stock market, Tadawul implemented a 15% index cap. No matter how large Aramco’s market cap grew, its weight in the benchmark index was restricted.

With the Dangote Refinery structurally designed to be worth about 46% of the NSE, the major question I have now is: Can Nigeria’s SEC or the CBN replicate any of those mechanisms?

The structural realities suggest they cannot. The SEC can mandate index capping alongside the NGX, but the Central Bank of Nigeria is in no position to instruct commercial banks to hand out cheap, leveraged retail loans for stock market speculation. If anything, the current CBN governor is focused on de-risking the banking sector and cleaning up balance sheets.

The race to participate in Africa’s historic IPO will very likely trigger a massive, cannibalistic sell-off across the rest of the NGX as the market scrambles to find liquidity. With Dangote targeting local funding and pension funds, and trying hard to avoid a repricing of the valuation by foreign markets, the die for who would be the exit liquidity seems to have been cast.

Conclusion

Being bearish in a market that keeps making new highs is a lonely trade. I cannot tell you when the music stops… because I don’t know. Plus, the fact that the market can stay irrational far longer than any investor can stay solvent is another reason I keep a long-only approach to investing.

However, much like the prelude to the 2007 correction, the Nigerian stock market is currently being hawked to everyone. Exit liquidity has to come from somewhere, and the everyday Joe is stepping up as the available sacrifice.

The FTSE re-rating is set to formally happen in September 2026, and Dangote is planning a July-August IPO. While I’m more concerned with the US market’s hope-as-a-strategy approach into midterms, I believe Q4 into next year will be very interesting to watch. Just that most of the retail market feels unprepared for it.

Hmmm…

This was a very insightful read for me. As a retail investor, I had never seen things from this angle. Thank you!